BetterBond

The impact of interest rate changes on the residential property market is predictable and has been vividly demonstrated by the latest reading of the BetterBond index of home loan applications. In reaction to the latest interest rate cut, which took the prime rate down to 10.5%, this index increased by 11% QOQ and by 14% YOY during July and August. In the process, the number of home loan applications reached its highest level since Q3 2022, when the record-high interest rates started biting into the pockets of prospective homebuyers.

The month in numbers

- 11% QOQ increase in the number of home loan applications

- R1.3 million – average FTB home purchase price

- 5% YOY decline in average deposit for all buyers

- 6.6% YOY increase in share of homes above R3 million sold

Average home purchase price

During July and August, the average home purchase price for all buyers managed to beat its previous record high by the smallest of margins, remaining just short of the R1.6 million mark.

For first-time homebuyers (FTBs), the average price during July and August climbed to a new record high of slightly more than R1.3 million. The YOY increase in the average house price for all buyers was just 1.2% – well below the current inflation rate of 3% – showing that the residential property market still favours buyers.

Since Q2 2023, when the residential property market went into a slump, the average house price for all buyers increased by 5.9% (in nominal terms), which is virtually on the nose of the change in the consumer price index over this period.

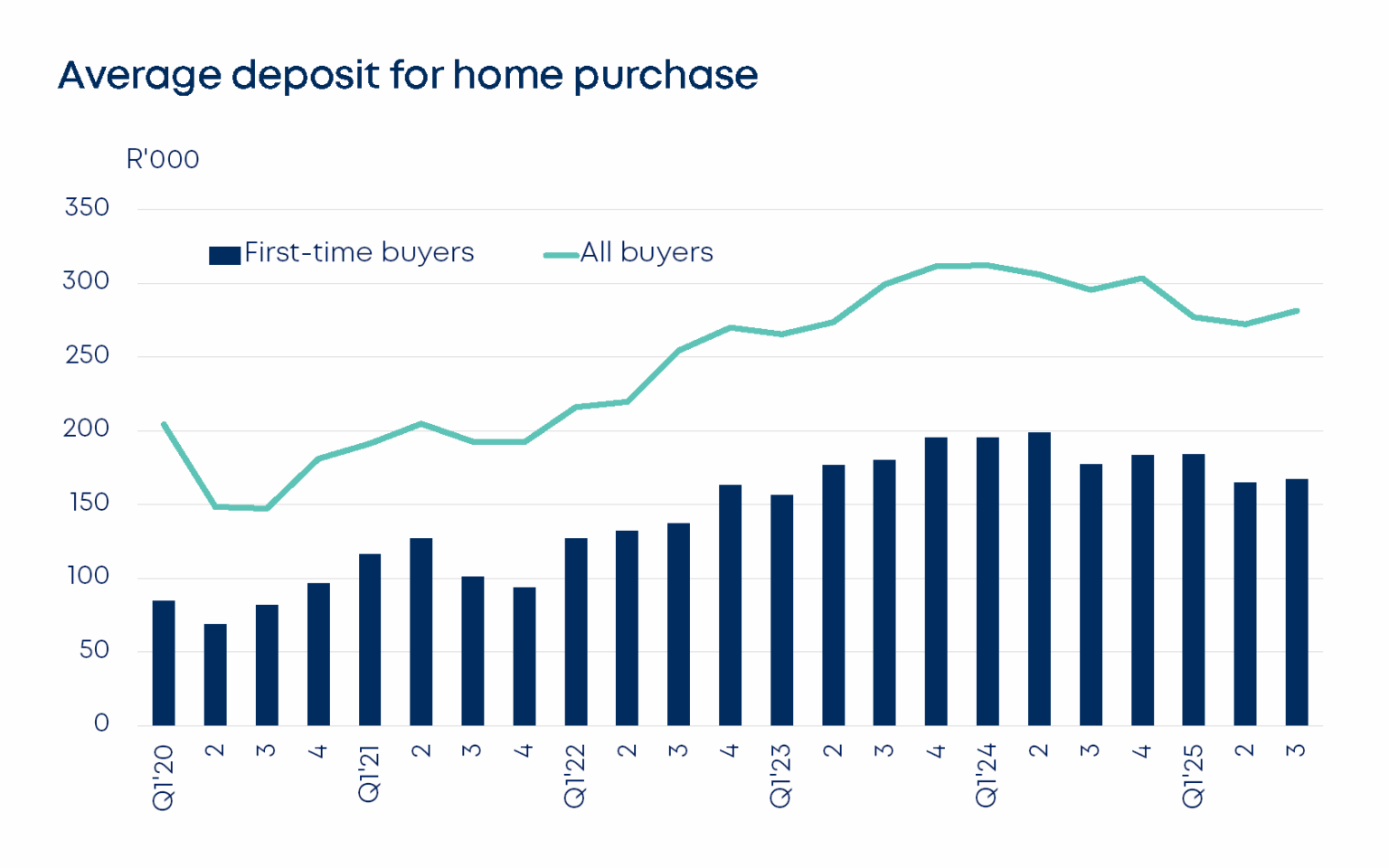

Average deposit for home purchase

Ever since Q1 2024, the average deposit required for home loans has been playing yo-yo, with a series of up and down movements. Fortunately for prospective homebuyers, the net effect until the end of August has been downward.

Although Q3 to date experienced another marginal increase in the average deposit (for all buyers and FTBs alike), the YOY figures showed declines of 5% and 6%, respectively. Due to the predictable increase in bank impairments because of the record-high interest rates between 2022 and the end of 2024, banks were compelled to raise their deposit requirements for mortgage home loans. The welcome reversal of this trend is bound to gather momentum if interest rates decline further.

Average annual deposit as a percentage of purchase price for all buyers since 2017

Between 2018 and 2021, the average deposit required for home loans (all buyers) by the banking sector was 14%. Due to the imposition of the South African Reserve Bank’s restrictive monetary policy, interest rates were raised to a 15-year high, which predictably led to a significant increase in the percentage of home prices that were required as deposits for loans. By 2023, the deposit level had been raised to 19.3% – representing an increase of 38% and making it more difficult for prospective homebuyers to purchase properties. Fortunately, the recent lowering of the prime lending rate to 10.5% has resulted in a modest decline in the deposit requirements (as a percentage of home prices), namely by 8%.

Read the full report here